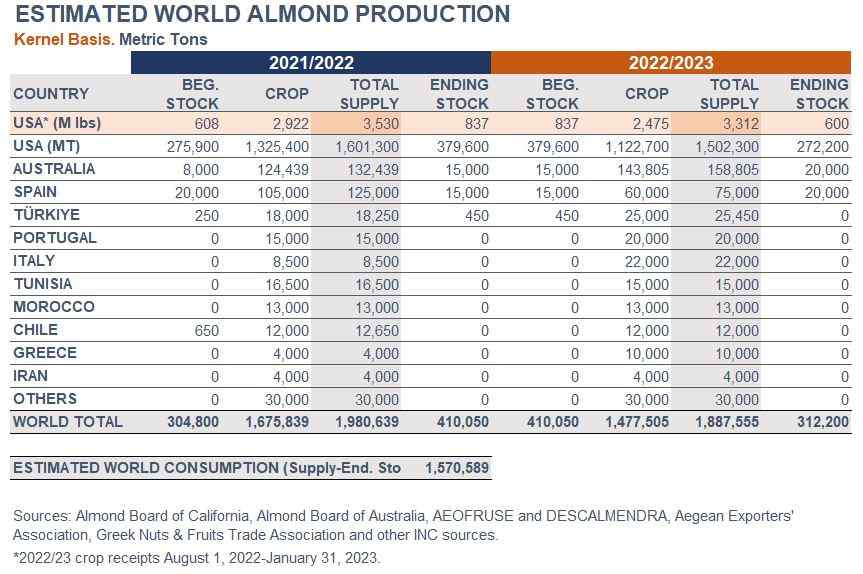

USA (California)

The January 2023 Almond Board of California Position Report shows receipts of 2.475 billion lbs. (approx. 1,123,000 metric tons) crop year-to-date (August through January), trailing the 2021/22 crop by 12.5% through the first six months. USDA receipts show an average inedible reject percentage of 2.1% which is up from previous crops. Total shipments added up to 1.271 B lbs. (576,789 MT), up 2.6% compared to the same period in 2021/22. Due to the smaller crop and increased shipments, the computed inventory was down 7%.

Domestic shipments August through January underperformed exports and were down 7.3% vs. CY 2021/22 at 363 M lbs. (approx. 165,000 MT). Exports through the first six months of CY 2022/23 were up 7.2% at 908 M lbs. (approx. 412,000 MT). Shipments to the Middle East/Africa and European regions were up 63% and 10%, respectively. Exports to India nearly matched the strong performance from a year ago, down just 2%, while the Asia-Pacific region was down 10%.

After a winter which began with increased precipitation, attention is now focused on the pollination period as market expectations are set for the 2023/24 crop.

Australia

The Australian 2022/23 almond season has been one of the most challenging for growers in many years. Wind and hail damage in various growing regions was followed by flooding due to unprecedented rainfall in many parts, especially the eastern growing districts. This restricted the amount of in-shell produced and increased the level of lower-quality product. A varroa mite incursion that locked down beehive movements thwarted growers in the state of Victoria —which produces 60% of the nation’s crop— to fully stock their orchards for pollination during August. The long-held question as to what is the optimal number of beehives required per hectare was put to the test with some larger growers being forced to stock at rates that were more than 50% below the usual 5-6 hives per hectare.

The Almond Board of Australia released its pre-season crop estimate for 2023/24 at 156,200 MT. This is an 8.6% increase on 2022/23 but well below previous industry expectations as new plantings come into higher levels of production. At the time of writing this report, kernel sizing looked to be up and harvest was expected to be 1-2 weeks late due to the largely mild growing conditions. The latest ABA planting survey reveals that the much sought-after Nonpareil variety remains 50% of the Australian crop although newcomers are exploring self-fertile alternatives to guard against ongoing concerns around the number of beehives available for pollination.

Spain & Portugal

Mainly due to last summer and spring unfavorable weather conditions, the 2022/23 Spanish production is estimated at 60,000 MT, down by 20% from the previous forecast of 75,000 MT. The Portuguese crop was also reviewed 20% down, from 25,000 to 20,000 MT. Regarding the 2023 Spanish crop, the early varieties were in full bloom by the end of February in most producing regions; damage by frosts and rainfall scarcity, remain a concern.

According to AEOFRUSE, total kernel and manufactured almond exports from Spain (August-December 2022) amounted to 65,684 MT, with shelled almonds accounting for 76% of the share. This amount represents an 11% decrease from the same period last season. While shipments to the traditional Western European market were down by 12% from 2021/22, from 59,985 MT to 52,967 MT; some other destinations saw a significant increment. Exports to the Middle East amounted to 2,566 MT, 71% up from 2021/22, with Türkiye adding up to 1,541 MT, three times over last year. Shipments to Northern Africa amounted to 1,096 MT, 61% up vs. 2021/22.