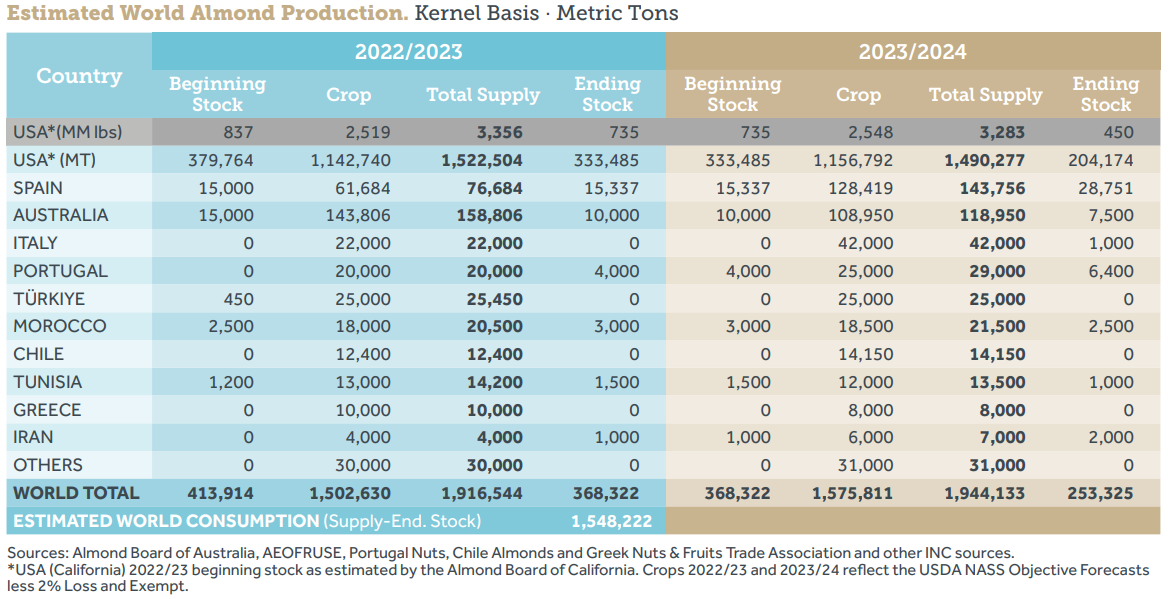

USA:

On July 12, the USDA NASS released its 2023 California almond objective forecast at 2.6 billion pounds (1.18 million metric tons), up 4% from May’s subjective forecast and 1% above last season’s crop. If reflecting a 2% loss and exempt, the 2023/24 crop is forecasted at 2.55 B lbs. (1.16 M MT). As discussed during the INC Congress in London last May, after the crop year 2020/21 high of 3.11 B lbs. (1.4 M MT), the forecast for the 2023/24 season is anticipated to be the second shorter crop year in a row, which is starting to ease some of the previous oversupply the Californian industry went through over the last few years. California bearing acres have been steadily growing over the last decade but have started flattening out over the last couple of years. Although above-average snowpack and rainfall have secured water supply for this year, water continues to limit new acres being planted.

As per the Almond Board of California Position Reports, total shipments year-to-date started off slow this season and it took until about mid-year for some of the export markets to start to pick up, with record numbers in January (+2.63% from 2021/22), February (+5.51%) and March (+6.85%). April and May YTD shipments were also up from 2021/22 by 3.49% and 0.25%, respectively; while June YTD total shipments of 2.38 B lbs. (1.08 M MT) saw a decrease of 3.51%. The initial ABC total shipment projection adds up to 2.78 B lbs. (1.26 M MT).

As COVID restrictions eased up in China, demand improved and was up by 17% YTD through June 2023 vs. 2021/22. The Middle East was a very important market this season (11% up), fueled by the favorable pricing reaching consumers. Europe was 10% off from last year’s number. The US market continued to lag and it remained to be seen if shipments would end up flat or slightly below last year.

All in all, the crop expected for the incoming season, combined with very strong consumption as well as a shorter Australian crop, puts the California almond industry in a favorable position to increase shipments and pull the carry-out into the 300-500 M lbs. (136,000-227,000 MT) range, which is very supportive for pricing.

Spain:

In spite of the drought currently affecting the producing regions, 2023/24 production —at the time of reporting— was expected to double vs. last year.

Based on the current planted area (761,662 hectares: 619,264 ha rainfed and 142,398 ha irrigated), production is foreseen to reach two times the current levels in the next five years. Bearing planted area adds up to 525,840 ha and organic production represents around 16% of the total share.

Australia:

Production in 2023 was 30% smaller than the pre-harvest estimate owing to weather disruptions from bloom until harvesting. Besides, the arrival of the bee pest Varroa destructor to Australia meant that there were issues in regard to hive movements on the eve of pollination.

After a ten-year sustained growth, in 2017 new planting reached a high of 7,000 ha per year. Currently, the total planted area, both non-bearing and bearing, adds up to around 65,000 ha and no significant growth is anticipated, mainly due to water availability. Based on hectares potentially topping out at around 70,000-75,000, production is anticipated to flatten out at around 200,000 MT. Since season 2020/21, water has been in abundance, but with El Niño looming, a new dry period can be expected.

The duty advantage into China and India has played well from a demand perspective. Unfortunately, this season, with Nonpareil tonnages down, fewer benefits were expected. After a decade-long growth, domestic demand has decreased 14% from its 2020 highs, to about 24,000 MT —down to just below the one kilogram per capita reached since 2015, as the inflationary pressure modified consumers’ discretionary spending.