Fertilizer Flows Resume, but Supply Relief Remains Gradual

Fertilizer shipments through the Strait of Hormuz have started to recover following the interim US-Iran deal, although flows remain far from normal levels, according to Reuters. Before the conflict, the strait handled around a third of globally traded urea and nearly half of seaborne sulfur, both key inputs for fertilizer production.

Since the deal was announced on June 15, around 640,000 metric tons of sulfur and 427,000 tons of urea have moved through the strait, according to data from the consulting firm CRU and the price reporting agency Argus cited by Reuters. This marks a clear improvement from wartime levels, but analysts cautioned that much of the cargo currently moving relates to older sales rather than fresh market supply.

The recovery remains fragile. More than 500 ships are still stranded in the Gulf, traffic remains well below pre-war levels, and empty carriers are not yet returning in meaningful numbers to collect new cargoes. Analysts said the waterway still needs to be cleared of war-related risks, while confidence among shippers will depend on whether the interim deal becomes a more durable truce.

A meaningful return to normal fertilizer flows may not happen before August, even under a best-case scenario. With some Gulf production facilities also damaged during the conflict, fertilizer markets may see only gradual relief, keeping input-cost uncertainty relevant for agricultural producers in the near term.

Brighter Signs in MENA as Oil Prices Ease and Resilience Holds

Oil prices in the Middle East and North Africa (MENA) region have declined to a four month low following peace talks and improving shipping conditions through the Strait of Hormuz, signaling a gradual normalization in Gulf energy supply, according to Oxford Economics. Kuwait, Iraq and Qatar have announced plans to restore production and export capacity, although operational disruptions and renewed geopolitical tensions continue to pose risks to the outlook.

Economic indicators across the region point to resilience despite recent volatility. Oman’s GDP grew by 2.6% in the first quarter, supported by stronger oil output and growth in agriculture and services, while Türkiye’s consumer confidence rose to its highest level since May 2023, reflecting improved household expectations and supporting domestic demand. However, analysts highlight that supply-side risks and infrastructure vulnerabilities remain, suggesting that the recovery path may be gradual.

Energy Risks Ease, but Asia’s Cost Pressures Remain

US-Iran de-escalation has reduced some of the immediate risks facing Asia-Pacific economies, particularly around fuel costs, but it is unlikely to fully resolve the region’s broader inflation challenge, according to a recent report by Oxford Economics. While oil prices have started to fall, a meaningful return of commodity flows through the Strait of Hormuz could still take weeks or months, with shipping and insurance costs likely to remain above pre-war levels for some time.

The report argues that the easing in fuel-related risks does not remove pressures elsewhere in the consumption basket. Earlier fertilizer shortages, high input costs and changes in planting decisions are expected to feed through with a delay, while El Niño adds a further weather-related risk to harvest outcomes in the coming months. Southeast Asia is highlighted as particularly exposed, given its vulnerability to yield losses and the large weight of food in consumer baskets.

The report also points to a more cautious monetary policy backdrop. Producer-price pressures, weak regional currencies and rising inflation expectations are expected to keep several Asian central banks on alert. Analysts still expect Indonesia, the Philippines, India and South Korea to maintain a hawkish bias, while Singapore, Malaysia, Thailand and Taiwan should have more room to remain on hold.

European Consumer Spending to Slow Amid Energy Shock

Consumer spending in Europe is expected to remain a key driver of economic growth in 2026, although momentum is likely to soften as higher inflation and weaker consumer confidence weigh on household spending, according to new analysis from Oxford Economics. The energy shock linked to the Iran conflict has reduced purchasing power and increased uncertainty, leading to a downgrade in consumption forecasts, with inflation-adjusted consumer spending growth in Europe expected to slow to around 1% in 2026.

The analysis highlights significant divergence across countries, with faster-growing markets in Central and Eastern Europe, the Nordics and Southern Europe outperforming larger economies such as Germany, France and the UK.

Despite these headwinds, resilient labor markets and solid nominal wage growth continue to support spending, while strong tourism activity is partially offsetting weaker real income growth.

Looking ahead, consumer spending is expected to recover gradually from 2027 as inflation pressures ease and confidence improves, although risks linked to energy prices and geopolitical tensions remain elevated.

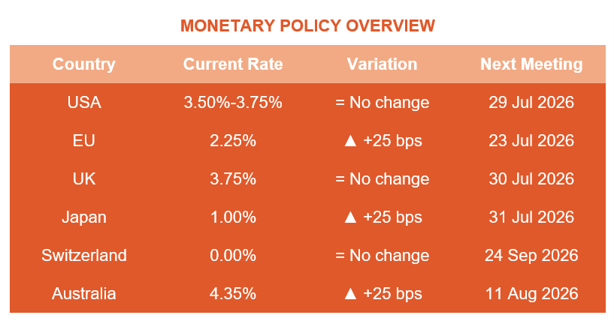

Rate Decisions Signal a More Restrictive Financing Environment

Recent central bank decisions point to a still-restrictive monetary policy backdrop, even as some institutions have chosen to pause. According to an EY report published on June 22, the Federal Reserve, Bank of England and Swiss National Bank kept rates unchanged, while the European Central Bank, Bank of Japan and Reserve Bank of Australia raised rates by 25 basis points.

Inflation remains the key concern across major economies, particularly where energy-related pressures risk spreading into broader price dynamics. The ECB raised rates for the first time in three years, taking the deposit rate to 2.25%, while noting that further action could depend on whether inflation proves persistent.

In the United States, the Federal Reserve kept rates at 3.50%-3.75%, but the report points to a restrictive policy environment, partly linked to the possibility of reduced balance-sheet liquidity under the new Fed leadership. In Japan, the Bank of Japan raised rates to 1.00%, the highest level in 31 years, as inflation pressures and yen weakness continue to affect import costs.

For global trade and corporate planning, the main takeaway is that borrowing conditions are unlikely to ease quickly. Higher financing costs can affect working capital, inventory decisions and investment across supply chains, particularly in sectors exposed to imported inputs, currency movements and uncertain demand conditions.