The Fertilizer Crisis: A Supply Chain Wake-Up Call

The near-closure of the Strait of Hormuz has sent global fertilizer prices to their highest levels since 2022, exposing a structural vulnerability in the agricultural supply chains.

How the Crisis Unfolded: The current fertilizer shock traces its origins to late February 2026, when hostilities in Iran led to the effective closure of the Strait of Hormuz to commercial shipping. According to the International Food Policy Research Institute (IFPRI), approximately 30% of global seaborne fertilizer trade and an estimated 20% of globally traded liquefied natural gas—a key feedstock for nitrogen fertilizer production—pass through the strait. Urea prices climbed above US$850 per metric ton in April, an increase of roughly 80% since February, according to the World Bank. In the US, anhydrous ammonia rose from US$828 per ton before the conflict to US$1,123 per ton by April 17, as reported by Farmdoc Daily (University of Illinois).

Impact on Key Growing Regions: In the United States, growers who had not pre-purchased nitrogen fertilizer before the conflict began facing sharply higher input costs during the spring growing season. A survey by the American Farm Bureau Federation found that 70% of respondents said fertilizer costs were so high they would not be able to buy all the fertilizer needed for the current season. In Europe and Türkiye, the shock has compounded pre-existing supply constraints linked to post-Ukraine restrictions on Russian and Belarusian fertilizer exports. Other areas that rely heavily on fertilizer imports and face similar pressures include India and West Africa.

Policy Responses: The EU suspended customs duties on key nitrogen-based fertilizers for one year on May 22, 2026, with an estimated savings of €60 million for EU farmers. In the United States, the FTC launched an industry-wide investigation into fertilizer pricing in late May. The USDA’s US$1.625 billion Assistance for Specialty Crop Farmers Program, open since June 1, provides bridge payments to tree nut and dried fruit producers partly in response to elevated production costs.

Outlook: The World Bank projects fertilizer prices to ease in 2027 as supply recovers, but flags upside risks if disruptions extend beyond the third quarter of 2026.

Oil Prices Stay Calm as Inventories Shrink and China’s Demand Remains Unclear

Global oil prices have remained relatively steady despite ongoing geopolitical tensions affecting key supply routes, including risks associated with the Strait of Hormuz, according to a recent analysis published by Reuters. Brent crude has been trading within a constrained range compared with broader historical price swings, even as market attention remains focused on potential supply disruptions.

The analysis highlights data showing a drawdown in global oil inventories, including declining stock levels in major storage hubs such as the United States. It also points to reduced seaborne crude imports into China, the world’s second-largest oil consumer, while noting that available data on Chinese domestic consumption and stockpiles is limited, making near-term demand assessment less clear.

The article further describes a market environment where price movements are occurring alongside uncertain signals about supply and demand balances. Traders are monitoring inventory levels, shipping flows and geopolitical developments closely, as these factors continue to influence expectations about future crude availability and pricing conditions.

In short, the market currently appears notably relaxed, despite the very real prospect of sustained disruption.

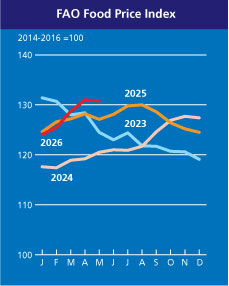

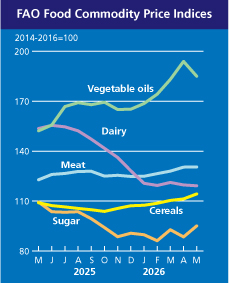

FAO Food Price Index Remains Stable Amid Diverging Commodity Price Trends

The FAO Food Price Index was broadly stable in May 2026, averaging 130.8 points, a slight month-on-month decline of 0.2%. While overall conditions were steady, underlying movements across commodity groups diverged. Increases in cereal and sugar prices were offset by declines in vegetable oils and dairy, while meat prices were largely unchanged. Compared with a year earlier, the index remains 2.9% higher, but still significantly below its March 2022 peak.

Among the main drivers, cereal prices continued to firm, rising 2.6% month-on-month on tighter wheat supply prospects, stronger corn demand, and higher input costs adding upward pressure on global grain markets. Sugar prices also jumped, reaching their highest level since October 2025 amid concerns over tighter future supply and shifts in Brazil’s ethanol-sugar allocation. In contrast, vegetable oil prices fell sharply, driven by weaker palm and soy oil quotations, while dairy prices eased further due to softer butter and cheese markets. Meat prices remained broadly stable, with gains in bovine and ovine meat offset by declines in pig meat.

Overall, the latest release points to a globally balanced environment with notable divergence across commodity markets. Weather conditions, energy costs, and biofuel dynamics continue to play a key role in shaping trends across individual markets.

Images: FAO

Wider Access to GLP-1 Medications Opens Up New Opportunities for Nuts and Dried Fruits

Recent developments point a clear global trend toward broader access to GLP-1 receptor agonists—the class of drugs better known by brand names such as Ozempic and Wegovy.

In 2025, the World Health Organization (WHO) added GLP-1 therapies to its Essential Medicines List for managing type 2 diabetes in high-risk patients, and later issued its first guideline on their use in treating obesity.

Momentum has continued into 2026. The first oral GLP-1 treatments are now emerging, marking a shift away from injections toward more convenient daily tablets and potentially expanding the number of people willing or able to use these therapies.

In May 2026, France became the first EU country to announce that it will reimburse the cost of Wegovy and Mounjaro prescribed to patients with severe obesity. In the US, the Centers for Medicare & Medicaid Services launched a new program expanding access for eligible beneficiaries starting in July, and CVS Caremark, which manages pharmacy benefits for roughly 90 million Americans, will start covering Eli Lilly’s GLP-1 medications later this year.

While coverage remains uneven and affordability challenges persist, the overall direction is clear: GLP-1 drugs are becoming more widely available across major markets. For the nut and dried fruit industry, this trend has important implications.

GLP-1 drugs mimic a natural hormone that slows digestion, stimulates insulin release and increasing feelings of satiety. Together, these mechanisms reduce appetite and lead many users to consume significantly less food.

As food intake declines, nutritional quality becomes increasingly important. Research indicates that individuals using GLP-1 medications may fall short of recommended intakes for several key nutrients, including fiber, calcium, magnesium, potassium, iron, choline, and vitamins A, C, D, and E.

This is where nuts and dried fruits offer a clear advantage. Naturally nutrient-rich and calorie-efficient, they deliver a concentrated mix of vitamins, minerals, healthy fats, and plant-based proteins into small, satisfying portions—making them ideal for people eating less but needing more nutrition per bite.

In an article in the American Journal of Clinical Nutrition, researchers urged clinicians to support patients using GLP-1 therapies in optimizing their diets by prioritizing nutrient-dense, minimally processed foods—including nuts, fruits and legumes, in addition to vegetables, whole grains, lean proteins and seeds. Their findings reinforce a central principle: when food intake is reduced, every bite needs to deliver greater nutritional value.

As GLP-1 use expands globally, the focus is shifting from simply eating less to eating better in smaller volumes. In that context, nuts and dried fruits are well positioned to play a meaningful role as compact sources of nutrition in an increasingly appetite-suppressed world.